Debunking the Myth Surrounding “Buying Term and Investing the Difference”

You’ve decided to purchase life insurance, and the next step is to determine what kind. Temporary needs are best suited to term life insurance, but how do you know if your need is only temporary? Insurance experts will often suggest that permanent life insurance could be applicable for everyone as the cash accumulation component can provide significant value even after the need for death benefit has declined.

On the other hand, financial pundits and consumer experts have suggested that the cash value potential of permanent life insurance policies is a poor tool for wealth accumulation. The alternative course most often suggested is to buy term life insurance and invest the difference in premium into the stock market.

Both approaches will have the ability to provide you with the death benefit protection that you want. There are significant differences as to what options you have at the end of the level term period, and you need to be aware of them. However, the discussion always comes back to what happens with the excess dollars that could be invested elsewhere.

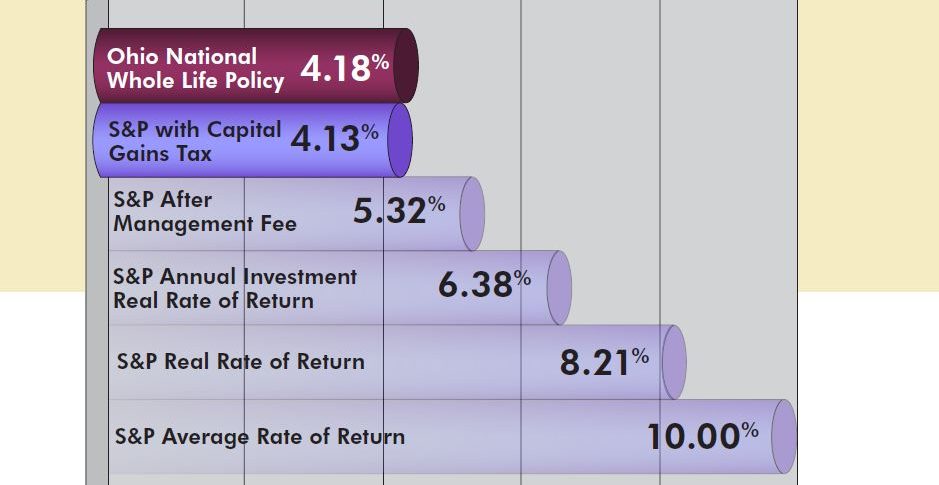

While it is impossible to predict the future course of any investment, we can test this hypothesis through the use of historical data. We know what the equity indexes produced in the way of historical returns. (See S&P 500 Index* returns at right.) We can look at that performance using some basic assumptions to determine how an individual might have seen their assets accumulate over time, either through permanent life insurance or through an investment.

Download the entire brochure here to find out more about….

- The “Buy Term and Invest the Difference” Question

- Average Rate of Return vs. Real Rate of Return

- Single Payment vs. Multiple Payments

- Managed Portfolio vs. Unmanaged Portfolio

- Taxed vs. Untaxed

- Twenty Years Later

- Debunking the Myth about Whole Life